THE FIRST GREEN BANK BACKSTORY

Ken LaRoe has always been an avid environmentalist and an avid capitalist. But he wrestled for many years with how to combine those twin impulses.

|

Ken LaRoe is a third-generation Central Floridian who grew up fishing, hunting, and generally immersing himself in the natural world on his grandfather’s citrus farm. He graduated with a degree in business from Florida State University in 1981 before the term social entrepreneurialism entered the popular lexicon, and spent the next 25 years living with a for-the-most-part suppressed desire to truly align his environmental values with his day job as a banker. After the successful sale of his third banking venture, Florida Choice Bank, to Alabama National Bancorp in 2006, LaRoe took a soul-searching, cross-country road trip with his wife, Cindy, and a gift from his brother, a copy of Patagonia founder Yvon Chouinard’s book Let My People Go Surfing. He returned with a determination not to compromise his values in his next banking venture.

In 2008 he filed an application with the FDIC for a new bank charter and opened First Green Bank in 2009. What he didn’t know at the time was how his definition of values-based banking would evolve and be enriched through his relationship with the Global Alliance for Banking on Values and his own tough-minded self-reflectiveness. The story Ken LaRoe would like nothing more than to say that it was his values proposition that convinced the FDIC to grant First Green Bank the last bank charter issued in the state during the darkest days of the 2008 financial crisis. He would also like to be able to tell you that it was his values commitment that attracted the investment capital that allowed the bank to open for business in 2009. But he knows otherwise. He knows that it had a lot more to do with his success as a traditional banker with his first startup: Florida Choice. “We sold Florida Choice in 2006, and our timing was fantastic,” he reports. “We had the highest multiple in the state of Florida, and our investors made a return of seven times their investment in six years. It was a big financial home run. So those investors came back because they had made money on their last investment with me. Frankly, most of them saw the green banking idea as just a good marketing idea. And the FDIC actually told me pretty early in the application process, ‘this is a niche bank and we don’t do niche banks.’ I just stayed on it and kept saying, ‘we are a bank, we will be no different than any other, but everything we do will be about environmental sustainability.’” As it turned out First Green Bank now aspires to be much more than environmentally sustainable. Ken has always been both an avid environmentalist and an avid capitalist. But he wrestled for many years with how to combine those twin impulses.

|

Managing Investor Expectations

Evangelical Minister and First Green Bank Board Member Joel Hunter"There has also been a certain amount of conflict on the board of directors and I see myself in a peacemaker role there."

David Raab, President of Roseville Farms & FGB Investor"Kenny has proven that values and banking are not mutually exclusive."

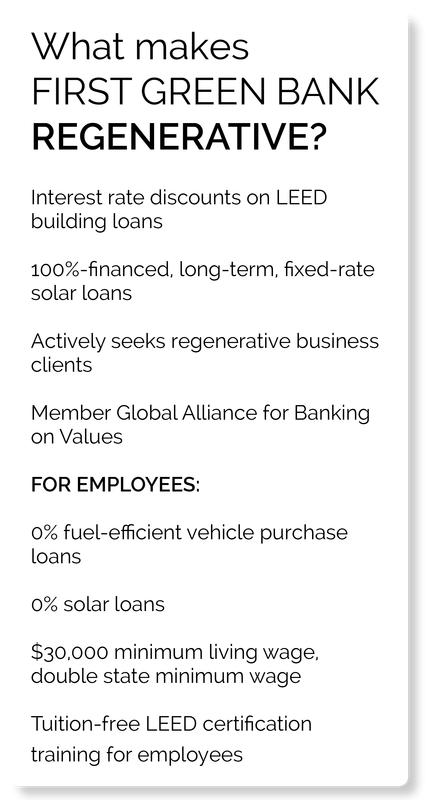

Jim Gissy, VP, Westgate Resorts and FGB investor“I like the idea that their focus is thinking about sustainability of the environment. What good will it do if the environment is screwed up? It won’t matter how much money you have.” With his new bank charter and fully capitalized in 2009, Ken set about in earnest to determine just what a bank based on values looks like and how he could adapt the model to the Central Florida business culture.“There have been a lot of “ah hah” moments, asking myself, 'are we worthy? What authorizes us to be a values-based bank?'” Ken admits. “It is that internal wrestling I am doing.”“We need to try to direct our deployment of assets into areas that at a minimum are not harmful. It is easy to say who we want to target, but more difficult to be exclusionary,” he notes.

Cultivating Regenerative Borrowers

Convenience Store Conversion

|

During the years he ran Florida Choice, he recalls, “it bugged me that we were financing all these development projects" that were decimating the central Florida landscape. So he did things “around the edges of environmental sustainability,” like converting the bank’s courier service to a fleet of hybrid electric cars, and being on the forefront of green building in the early years of LEED standards, retrofitting branches for energy efficiency. “But the truth is I felt a lot of resistance from shareholders when I expressed a desire to go deeper and I was scared to push it,” he admits.

After he sold Florida Choice and returned from his epiphanic cross-country odyssey, Ken decided that at long last he was ready to rock the boat. “I wanted to be impactful,” he maintains. “When I started up First Green Bank I didn’t really know what I meant by no compromise, but it was going to be, ‘if I say we are going to do this we will.’ I told my directors up front this is the way I want to be. A couple joined strictly because of that. One of my board members, my pastor, Joel Hunter, would not have considered being on a bank board if it weren’t for that. That started the evolution for me.” With his new bank charter and fully capitalized in 2009, Ken set about in earnest to determine just what a bank based on values looks like and how he could adapt the model to the Central Florida business culture.

I had to educate myself from a foundational level,” he says. “I found Triodos Bank through a Google search. The Global Alliance for Banking on Values was just being formed at that time and I started reading about that, too.” He befriended Vince Siciliano, the CEO of New Resource Bank in San Francisco, and Tamara Vrooman of Van City Credit Union, both GABV members. Tamara invited him to GABV’s annual conference in Vancouver in 2012 and the pace of his journey to understand what values-based banking was about accelerated when First Green Bank became a full GABV member. Ken says he is constantly being challenged by his GABV affiliations and other relationships he has sought out over the past few years, notably with Florida’s gay community through his new friendship with Trevor Burgess CEO of St. Petersburg-based C1 bank. “There have been a lot of “ah hah” moments, asking myself, 'are we worthy? What authorizes us to be a values-based bank?'” Ken admits. “It is that internal wrestling I am doing.” As a GABV member, First Green Bank is beta testing the organization’s new scorecard self-assessment tool. It has been a sobering experience, Ken relates, and has often required incredibly granular, but critical, operational changes at the bank. “We ended up doing a manual scrub of our entire loan and deposit portfolio and realized we don’t have any basis to determine where our business was or wasn’t mission-aligned because our existing core processing software did not track it.” While New Resource shared an exhaustive checklist that all its customers are required to fill out, Ken knew “we would just have a mutiny on our hands if we tried to do that in Central Florida.” It took months to come up with a distilled version that would capture what was required, a simple one-page checklist for customers. “For the last 24 months we did a core conversion change and we chose our current software provider because it allows us to track the mission- alignment component of our customer base,” he says. “So in a couple of months every new loan will be coded at the time of inception and we can slice and dice the data.” But having the software in place to capture values-based lending practices is one thing and finding values-based borrowers to lend to in Central Florida is quite another. First Green Bank has been working hard to extend loans to enterprises like King Grove Organic Farm, Alfredo Avila’s Deland Organic Bakery, and a family business that has rehabilitated Wekiva Island. But lending to regenerative businesses like these still makes up only a small portion of the bank’s loan portfolio. “We are located in the county I was born and raised in, which was historically completely agrarian,” Ken relates, “but when we had the back-to-back freezes in the 1970s and 1980s it killed the citrus industry. Now the main business is condos, strip malls, motels and convenience stores, and we have been lending to these businesses because we have to stay alive and meet shareholder expectations. So far we have not disappointed, our financial performance has been very good and our credit quality is number one in the state every quarter," he notes. "We continue to target values-based, mission-aligned customers and borrowers and working hard to educate. But we are not there yet.” Balancing the sometimes conflicting demands of meeting shareholder expectations, the regulatory requirements of a de novo bank, and fulfilling its values-based mission has forced Ken to get creative. That, and the very scarcity of businesses that are closely-aligned with First Green Bank’s mission is forcing the bank to think outside of the box. For example, the bank lends to many convenience stores, flagged by an Exxon or 7/11, that, as Ken say, essentially sell “carbon-based dirty energy and junk food.” He has approached many of these stores to extend financing to them for solar arrays. And, noticing on a recent trip to Nashville that some of the convenience stores in that city are featuring a whole new concept with healthier food choices, he reports he is contemplating suggesting to one of his larger borrowers that they convert one or two of their stores to this model, with financing from First Green.

Ken’s next big push will be to work with his board to create a set of policies for the types of businesses the bank will not lend to. “We need to try to direct our deployment of assets into areas that at a minimum are not harmful. It is easy to say who we want to target, but more difficult to be exclusionary,” he notes. “Fracking is easy, water bottling, extractive industries are easy, gun manufacturing is easy, or a water park. Not so easy is deciding, will we do slash and burn residential development going forward?”

|

“As a member of the GABV board of directors I am exposed to things I was never exposed to before—the Bangladesh lender that does 8,000 micro-loans per month, Sunrise Banks in Minnesota that wants to bank the unbanked and break the back of the payday lenders. I am receiving great ideas and hanging out with these great people.”Banking the Unbanked

|

Ken has recently raised his aspirational bar to new heights as he connects with an even deeper understanding of what a holistic-value bank could and should be. He is now looking to infuse First Green Bank’s environmental mission with a social one—a goal that few banks that call them sustainable can now say they have achieved. “I knew about the issues around social equity but it wasn’t something that propelled my interest prior to my association with GABV [he was elected to the GABV Board of Directors in 2014],” he says.

Ken notes he is being cheered on by his fellow GABV members who operate in parts of the country that are much less challenging for values-based banking and/or that are not operating under the regulatory restrictions a de novo bank is subject to. “They tell me not to beat myself up,” he reports. “I know they are right, that I have to work with what I have and be positive and incrementally create my own community.” “As a member of the GABV board of directors I am exposed to things I was never exposed to before—the Bangladesh lender that does 8,000 micro-loans per month, Sunrise Banks in Minnesota that wants to bank the unbanked and break the back of the payday lenders. I am receiving great ideas and hanging out with these great people.” First Green Bank now has a branch in South Orlando where there are some lower income census tracts, so there is theoretically an opportunity to provide services to the unbanked in this community. But again, the challenges are considerable. “I am now constantly wrestling with how to do that, but it is a difficult market to serve,” LaRoe notes.

As a de novo bank First Green is subject to very strict regulatory scrutiny and must adhere to stringent credit quality restrictions. “We are discouraged from lending to someone with a credit score under 650,” Ken reports. “Even lending on the home mortgage side, with Dodd Frank, the regulatory burden is overwhelming. It has taken vast amounts of community banks out of home lending. We are trying but you can’t make exceptions anymore, you might want to lend to someone who had a credit hiccup during the meltdown and give him a break, but you can’t do it.” Ken says he is thinking of things that the bank could do in its financial holding company that would not be possible to do on the regulated banking side to address social equity. He is in talks with David Reiling, CEO of Sunrise Banks, brainstorming collaborations they might undertake together, adapting some of the financing tools Sunrise has created to serve its own low-income communities. “To break the backs of payday lending is not something we will retreat from,” Ken maintains. “We will keep trying to figure out how to address it.” Ken maintains that he is so energized by the challenges before him that he feels he has reached “the pinnacle of Maslow’s hierarchy of needs.” “I am close to self-actualization,” he reports, “and I never thought I would get there. This is really special.” |